After the Chips, the Robots

The Next AI Trade: Physical AI and Humanoid Robotics

For three years, the Artificial Intelligence trade had only one address: semiconductors.

Nvidia and the accelerated computing ecosystem absorbed almost all thematic capital, based on the correct thesis that without computing power, no model can exist. That phase is not over, but it is maturing.

This analysis, built on the observation of flows and supply chain microstructure, formalizes what positioning was already signaling: the next leg of the AI trade is shifting from infrastructure (chips) to physical-world applications, and the most legible monetization frontier is humanoid robotics.

Our thesis is not a bet on a single robot. It is a thesis on the supply chain: our preference goes to high-value components harmonic reducers, actuator assembly, planetary roller screws because they possess higher technological barriers and a greater certainty of adoption compared to the finished product. The operational message is clear: expose yourself to the "picks and shovels," not the gold miners. And do so in Asia, where the same growth profile trades at a ~21% discounton the median compared to US peers.

From Digital to Physical: The New Data Bottleneck

The first wave of AI was digital: text, images, code. The bottleneck was computing power, and the winner was whoever sold that computing power. The second wave moves intelligence into the physical world a robot that grips, moves, inspects and here, the bottleneck changes nature. It is no longer (only) computing power: it is physical data.

Unlike Large Language Models, which found a ready-made ocean of text on the internet, robotics models require force, torque, and movement data that simply do not exist at scale. Compensating for this scarcity has become the central problem of the industry.

Fieldwork within the Chinese ecosystem reveals a picture of rapid architectural maturation but still embryonic commercialization. The technical debate has shifted from standalone VLA (Vision-Language-Action, or "I see, I understand the command, I act") models toward richer multimodal stacks:

VTLA models add touch where physical contact matters.

World models which predict the next state of the environment serve as a planning and validation layer for the action before it is executed.

Model scales are currently growing toward 40–80 billion parameters.

This is the conceptual difference distinguishing this phase from the previous one. The "chip" phase rewarded whoever provided the computing power. The "robot" phase rewards whoever can acquire high-quality physical data at scale via centralized data factories or distributed, egocentric, and human-centric collection and whoever provides the high-precision hardware components that make contact with the real world possible. This is where investable value is concentrated today.

The Commercial Stage

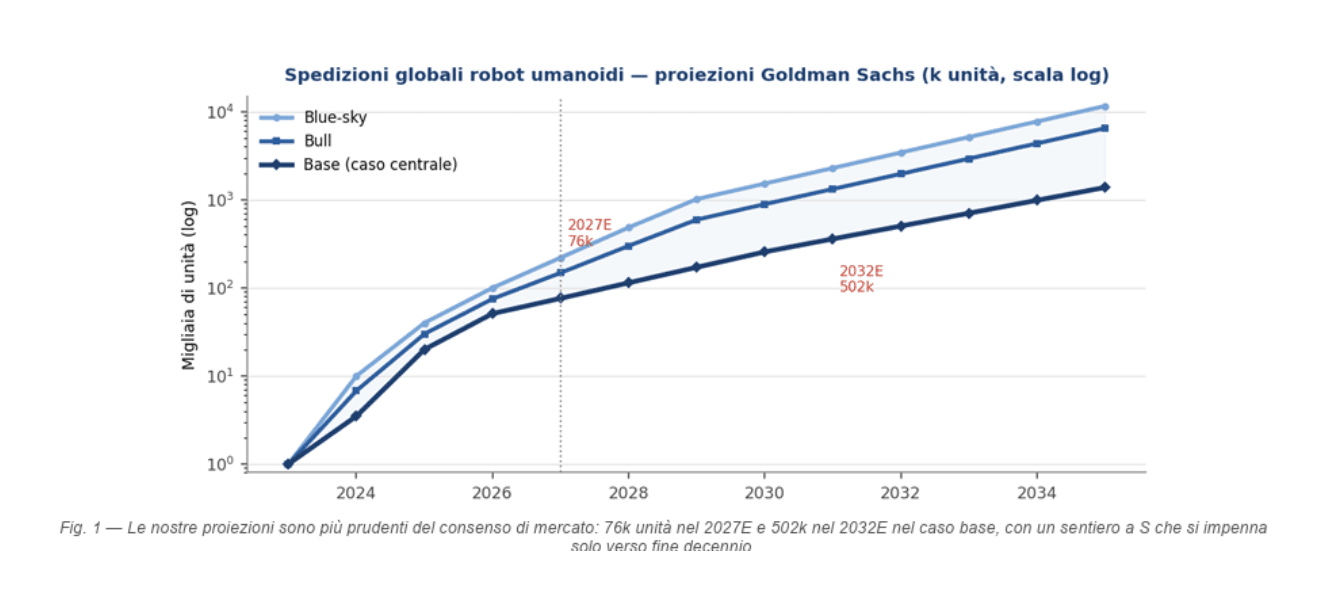

Commercialization is still in its infancy. Most applications are at the proof-of-concept stage, particularly in industrials and logistics; large-scale deployment is expected between 2027–2029, once tens of millions of hours of quality data have been accumulated onto a deployment-ready model.

The most concrete short-term opportunities lie in standardized tasks: sorting, material handling, pick-and-place, and inspection. Furthermore, we note that due to cost constraints and model capabilities, many operators currently prefer a mobile base robot with a 2-3 finger gripper—sufficient to cover 70–90% of industrial applications—postponing the adoption of bipedal humanoids with five-finger hands.

The Four Pillars of the Thesis

Our thesis rests on four pillars that, taken together, explain why we consider this an early-cycle entry point and not an already priced-in theme.

1. The Ultimate Endpoint Market

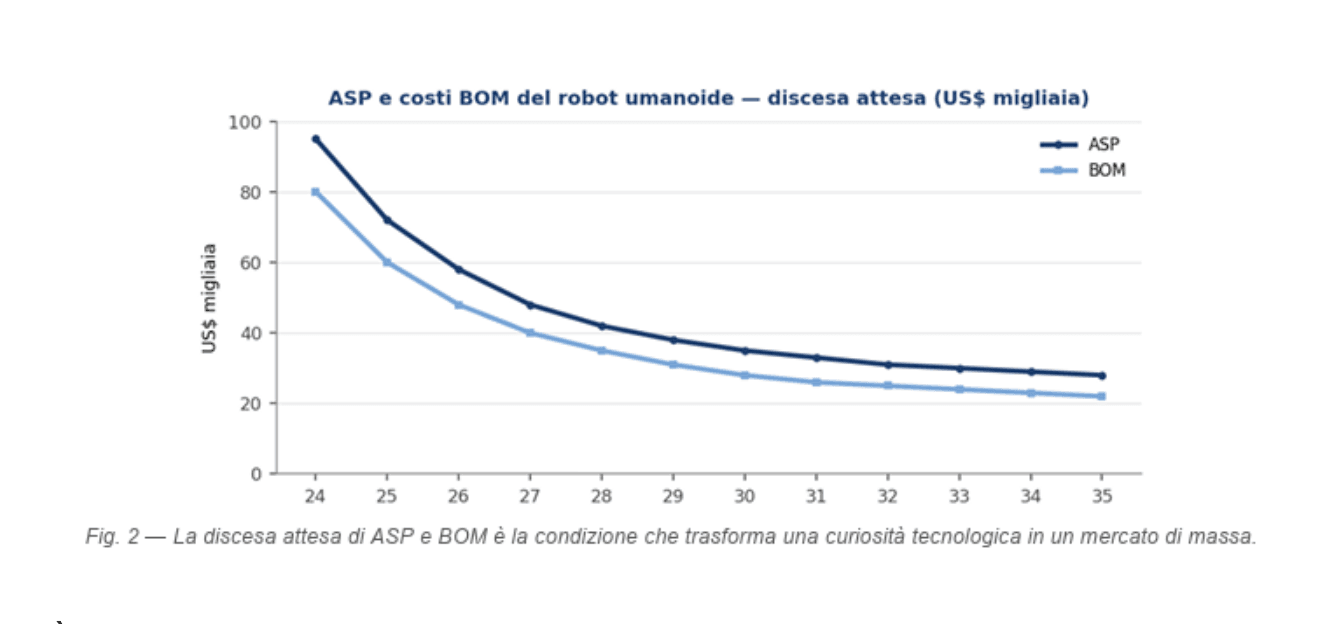

Behind our constructive view is the hypothesis that the humanoid robot could become the next widely adopted terminal device after smartphones and cars. The drivers are two-fold: structural tailwinds (labor shortages, automation demand) on one side, and the deflation of ASP (Average Selling Price) and BOM (Bill of Materials) on the other, which improves product economics as scale grows and R&D control becomes full-stack.

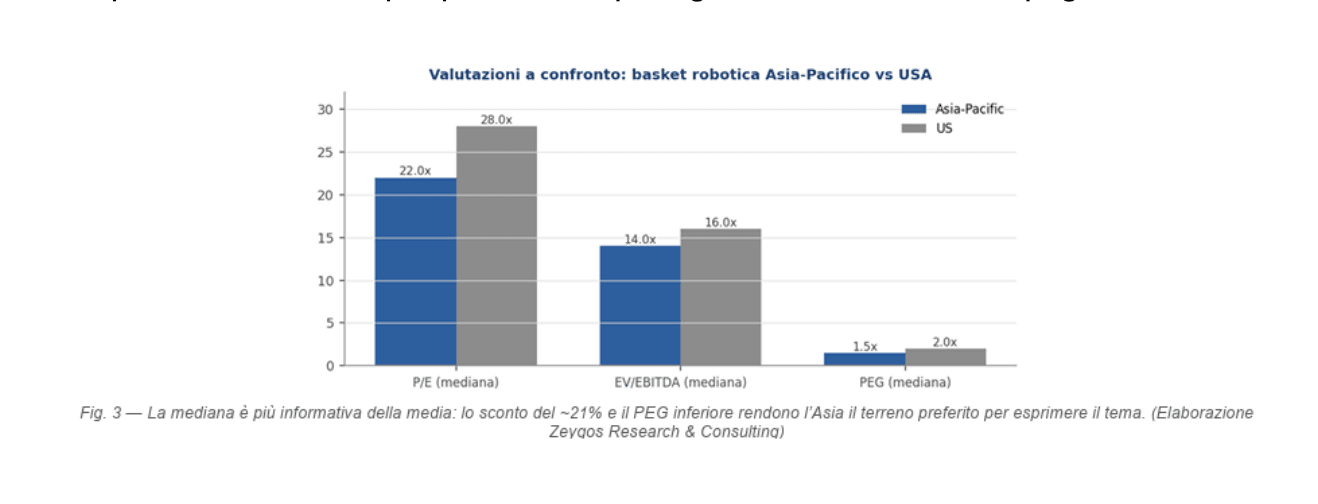

2. Valuation Dislocation: Asia vs. USA

This is the most actionable pillar. On an average basis, the two baskets—Asia-Pacific and the United States—appear similar (~29–30x P/E). However, the median tells a completely different story: 22.0x in Asia versus 28.0x in the US.

The typical Asian industrial/robotics stock trades at a ~21% discount to its American counterpart. While the Asian average is inflated by outliers such as Leader Harmonious Drive (~95x) and Harmonic Drive JP (~85x), the more representative median indicates that the Asian PEG ratio (1.5x) beats the US PEG (2.0x). Simply put: in Asia, you buy more growth per unit of valuation paid.

3. Institutional Flows and Passive Rebalancing

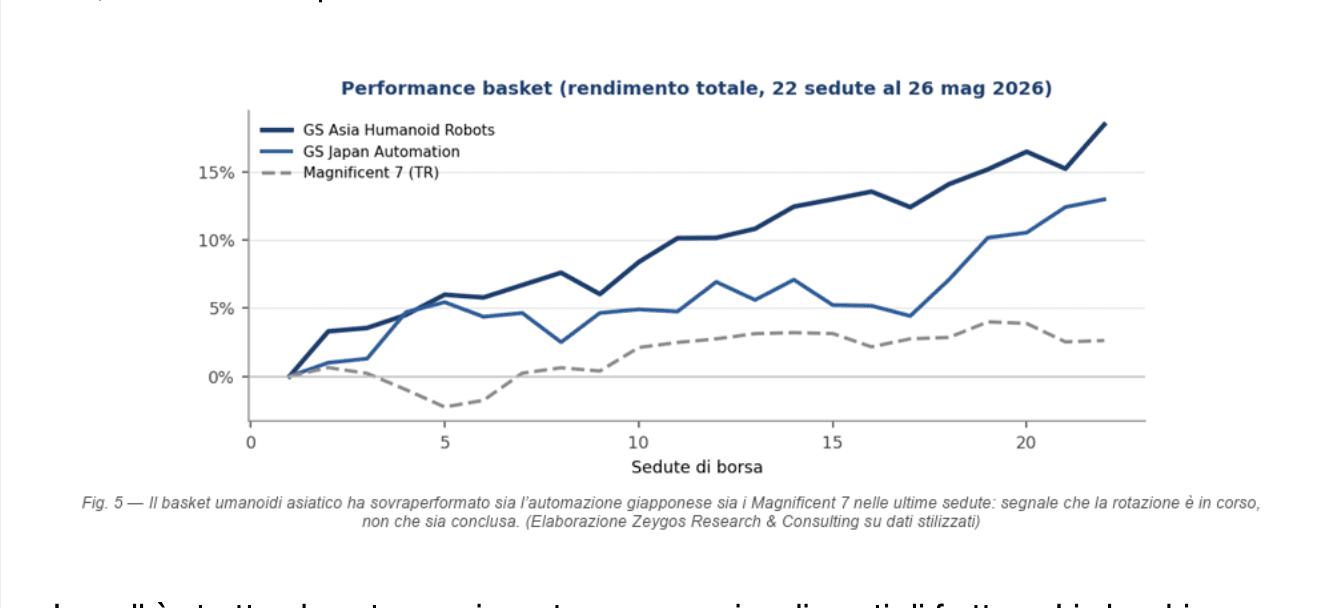

Mutual funds have begun rotating toward robotics-related supply chains, but positioning remains early and concentrated on components rather than pure-play robots. Flows are moving toward Korean and Chinese auto components, Chinese industrial automation and precision manufacturing, and selected robotic component suppliers.

Passive rebalancing is also driving a sharp rotation in Korea (inflows into Mobis vs. outflows from Hyundai Motor), while Japanese industrial automation is experiencing widespread passive selling, with an amplified price impact on mid-caps.

4. Near-Term Catalysts and Nvidia's Physical AI Ecosystem

The inflection point the moment when robots become "good enough" at 5–10 generalized tasks, with high success rates and rapid reasoning remains undated. However, the calendar offers concrete catalysts: the launch of Tesla Optimus Gen 3 and the publication of 2026 order/shipment targets by companies in the sector.

On the enabling front, Nvidia’s Physical AI ecosystem (Jetson Thor for edge computing, the GR00T foundation model, the Isaac platform, and Cosmos tools for generating synthetic data) acts as the primary accelerator: it is how the industry bypasses the scarcity of real-world physical data.

Component Deep-Dive: Where the Value Accumulates

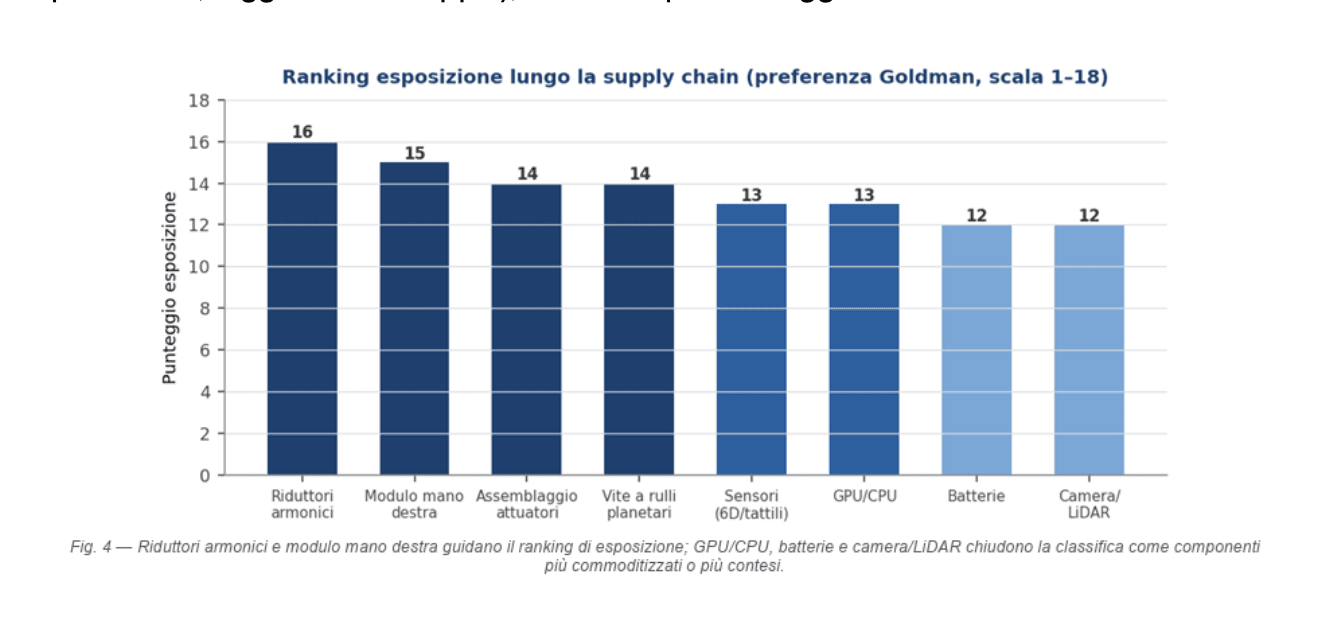

The operational heart of our thesis is a preference for high-value components. We classify exposure across eight component categories based on BOM content, technological barriers, capacity flexibility, and incremental opportunities stemming from humanoids.

At the top of the ranking are harmonic reducers and actuator assembly: the former for higher growth potential (high barriers regarding precision, lightweight design, and torque), the latter for greater certainty of adoption.

Two dynamics deserve close attention:

Actuator Assembly: Companies building cars and developing robots (led by Tesla) will need to rely on Asian suppliers and will require an intermediate assembler to manage relationships with various component vendors. This role carries low risk regarding hardware configuration changes. We expect a market share split of 70%/30% in favor of Sanhua over Tuopu (revised from a previous 50/50 split), citing Sanhua's dominance in EV thermal management modules within Tesla.

Harmonic Reducers: Harmonic Drive System remains dominant (~70%), but LeaderDrive is gaining ground (~30%, up from 20%) thanks to competitive pricing and flexible capacity, with a long-term split expected to settle around 50/50.

Prudence is required for more uncertain components. The planetary roller screw landscape is rapidly shifting: Schaeffler holds a track record advantage (estimated 50–60% share), but production yields, consistency, and capacity readiness remain the variables that will decide the long-term winner, who is unidentifiable today. Regarding the robotic hand, the technological roadmap remains wide open—with architectures ranging from 11 to over 20 degrees of freedom—making single-stock selection highly risky.

Mapping the Listed Universe

In line with this framework, we exclude the numerous private companies in the ecosystem (such as Agility, Daimon, Figure, Galaxea, Galbot, Spirit AI, Unitree, etc.). While technologically relevant, they are effectively uninvestable in public markets at this stage.

Cross-sector enablers should not be overlooked: Nvidia (NVDA) as a supplier of chips and Physical AI foundation models; Keyence (6861.T) and Fanuc (6954.T) as pillars of Japanese automation; CATL (300750.SZ), Samsung SDI (006400.KS), and Panasonic (6752.T) on the battery front. In sensors, Vishay Precision (VPG) and Novanta (NOVT)offer Western listed exposure to torque/force and vision.

Three Ways to Play the Theme

There are three ways to express this theme, in increasing order of idiosyncratic risk:

a) Basket / ETF Approach: For those wishing to allocate once and diversify single-stock risk, the cleanest path is a basket. Defiance has filed for a China Robotics ETF—a vehicle that, once operational, would offer diversified exposure to the Chinese supply chain. In the absence of an already available listed product, an equally-weighted basket of listed enablers replicates the idea while minimizing selection risk.

b) "Picks and Shovels" Approach: Overweight high-barrier components (harmonic reducers, actuator assembly) and underweight finished robot manufacturers, which are still pre-revenue and priced on pure optionality. The logic is simple: the supply chain collects revenue regardless of which robot brand ultimately wins.

c) Asia vs. USA Relative-Value Approach: Capitalize on the ~21% valuation discount by going long on the Asian basket, potentially with a partial hedge on the more expensive US basket. This is the most direct way to monetize the valuation dislocation identified in our analysis while reducing directional exposure to the theme.

Risk Factors and Friction Points

While the call is structurally compelling, it is not without friction points.

We list them in order of relevance:

Supply-Demand Mismatch & Structural Overcapacity: Chinese suppliers are building capacity for 100k–1 million units/year using a "capacity-first" strategy, even without confirmed firm orders or definitive timelines. With global shipments estimated at 1.38 million units only by 2035, the risk of overcapacity and margin compression is real if demand from anchor clients (primarily Tesla) delays. It is a high-stakes bet on future demand.

An Undated Inflection Point: A generalist AI robot remains a technological challenge for the coming years. Without an event demonstrating reliability and reasoning across multiple tasks, the market may lose patience. Valuation is highly sensitive to both the shipment outlook and the exit multiple (typically 40x, but soaring up to 120x during euphoric phases, as seen with Chinese EVs between 2009 and 2012).

Open Hardware Roadmaps: For robotic hands and planetary roller screws, the long-term winner remains undefined. Betting on the wrong component can wipe out optionality. Hence, our preference for assemblers and harmonic reducers, where adoption is more certain.

A Crowded, Theme-Driven Market: Supply chain stocks have been driven by narrative since 2022. A cooling of the AI narrative or a reallocation of systematic positioning could hit the most expensive names before the more defensive ones. The Asian discount acts as a relative protection, not an absolute one.

Conclusion

My reading does not suggest that the robots have arrived. It indicates that capital is beginning to rotate toward them, and that the smart way to participate in an early-cycle phase is through the high-barrier supply chain in Asia, where the same growth costs less.

The stage is still one of proof-of-concept; mass deployment is a matter for 2027–2029; the bottleneck is physical data, not silicon. For the investor, this translates into three practical guidelines: prefer components over finished robots; prefer Asia over the US for equivalent growth; and monitor the two catalysts that will validate or invalidate the thesis—Optimus Gen 3 and 2026 order targets. As long as capacity runs ahead of orders, risk discipline remains the primary position in the portfolio.